Loan-to-Value and Combined Loan-to-Value ratios are used to evaluate the total amount of a property that is encumbered by liens and debt obligations.

Understanding how providing a loan to a borrower relates to the value of the property or asset the loan is for shows a lender whether this is a good deal or not. For instance most lenders impose a LTV ratio max of 80%, to ensure that they gain 20% upside in case the loan defaults.

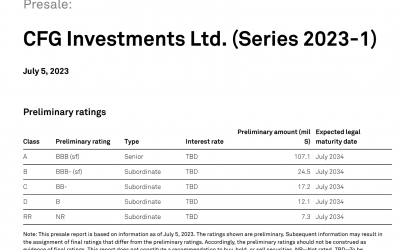

Loan-to-Value Ratio

To get the LTV ratio you simply divide the loan by the value of the property or asset the loan is collateralized against.

In this example of a property purchase:

Property Value = $100,000 USD

Down Deposit = $40,000 USD

Loan Amount = $60,000 USD

The LTV ratio is, the loan amount divided by the property value, 60%.

Here the lender is fine with this loan, knowing that for their loan, they are seeing a 40% upside in case they default.

Combined Loan-to-Value Ratio

This combined LTV ratio is the same as a standard LTV ratio, but takes in multiple loans against one property. This ratio is used in the case of second mortgages, or getting a second loan against an asset or property.

To get the LTV ratio you simply divide the sum of all the loans by the value of the property or asset the loan is collateralized against.

In this example of a getting a second mortgage:

Property Value = $100,000 USD

Existing Loan Amount = $60,000 USD

New Additional Loan Amount = $10,000 USD

The Combined LTV ratio is, the sum of the loan amounts divided by the property value, 70%.

Here the second lender is fine with this loan, knowing that for their loan, their loan is secure in case they default.

Why CLTV and LTV Matters

Prospective buyers may choose to lower their down payment by receiving multiple mortgages on a property, which means a lower loan-to-value ratio for their primary mortgage. You still want to ensure that no matter your financing structure you are not over leveraging yourself and putting your asset at risk.

Understanding this metric and making sure you stay on a target allows you to make a better purchasing decision.

This metric is important for lenders to see if providing a loan is a good decision, and is important for a buyer to ensure that they are not taking on too much debt and risk. When making a financial decision, being as informed as possible is key to ensuring the right course of action is taken.